Time-loss benefits in Oregon are what stand between an injured worker and an empty bank account while they recover. When a job injury keeps you off work, these payments replace a portion of the wages you are missing. But the rules around how much you receive, when payments start, and how long they continue confuse almost everyone, and that confusion is exactly where insurers underpay or cut off benefits early. Understanding how time-loss works lets you check whether you are actually getting what Oregon law provides.

This guide explains how time-loss benefits are calculated, the waiting period that delays your first check, the different types of wage benefits, and the reasons payments stop. At Schoenfeld & Schoenfeld, we help injured workers across Hood River, The Dalles, and Eastern Oregon get the time-loss they are owed and challenge insurers who shortchange them.

Also Read

- When Insurance Denies PIP Medical Benefits

- Oregon Workers’ Compensation Survivor Benefits

- How We Help Injured Workers Secure Benefits

TL;DR

Time-loss benefits in Oregon are temporary wage-replacement payments for workers who cannot work because of a job injury. They pay two-thirds of your gross weekly wage at the time of injury, up to a maximum set by the state and adjusted each year. There is a three-day waiting period, so you are not paid for the first three days unless you are hospitalized as an inpatient or remain off work for at least 14 days. Your doctor must authorize you to be off work for time-loss to be paid. If you return to lighter or part-time work, you may receive reduced temporary partial disability instead. Payments end when you are released to regular work, return to work, or your claim closes. Underpaid and wrongly stopped time-loss is one of the most common disputes in Oregon claims.

Key Points

- Time-loss replaces lost wages. It pays you when a work injury keeps you off the job, not for the injury itself.

- The rate is two-thirds of your wage. Time-loss equals about 66.67% of your gross weekly wage at the time of injury.

- A maximum applies. Benefits are capped at a state-set maximum that is adjusted annually.

- There is a three-day waiting period. You are not paid for the first three days unless hospitalized or off work 14 days or more.

- Your doctor controls eligibility. Time-loss is paid only while a physician authorizes you to be off work.

- Light-duty work changes the math. Returning to reduced work may convert full time-loss into partial benefits.

- Payments are not permanent. They end at release to regular work, return to work, or claim closure.

- Mistakes are common. Miscalculated wages and early cutoffs are frequent and worth challenging.

Not sure your time-loss checks are correct? Underpayment is more common than you would think, and it is fixable. Schedule a complimentary consultation and we will review how your benefits were calculated.

What Time-Loss Benefits Are

Time-loss is Oregon’s term for temporary disability benefits, the wage-replacement payments you receive while you are recovering and unable to work. They are distinct from medical benefits, which cover your treatment, and from permanent disability awards, which compensate lasting impairment after your claim closes. Time-loss is meant to keep income flowing during the temporary period when your injury keeps you off the job.

These benefits flow from Oregon’s workers’ compensation law in Chapter 656 of the Oregon Revised Statutes and the administrative rules that implement it. The Workers’ Compensation Division describes time-loss as payment for the wages you lose when an accepted injury prevents you from working.

One point surprises many workers: time-loss is generally not taxed the way regular wages are, but it also does not replace your full paycheck. It is designed to cover a defined share of your lost earnings, which is why understanding the exact calculation matters.

How Much Does Workers’ Comp Pay in Oregon?

The core formula is straightforward. Time-loss pays two-thirds of your gross weekly wage at the time of injury, roughly 66.67%, up to a maximum amount set by the state. The Oregon Department of Consumer and Business Services explains in its time-loss FAQ that the benefit is based on your wage at the time of injury and capped at a statutory maximum.

The detail that trips people up is the wage calculation itself. Your “wage at the time of injury” can include more than your base hourly rate. Overtime, tips, bonuses, board, lodging, and second jobs can sometimes factor in, depending on your situation. SAIF’s overview of payments for lost wages walks through how the wage figure drives the benefit. If an insurer calculates your average weekly wage too low, every single check is short, which is why this number is worth scrutinizing.

The maximum and minimum time-loss rates are adjusted each year, so the cap that applied last year is not the cap that applies now. For an injured worker, the practical takeaway is to verify two things: that the insurer used the correct wage, and that it applied the current year’s figures.

The Three-Day Waiting Period

Oregon does not pay time-loss from the very first day off work in every case. There is a three-day waiting period, and how it works catches many workers off guard. Under the state’s administrative rule on the waiting period, you are not paid for the first three calendar days of disability unless one of two things happens.

You become eligible for those first three days if you are admitted to a hospital as an inpatient, or if you remain totally disabled and off work for at least 14 days. In other words, if your doctor releases you back to work within the first 14 days, you typically do not get paid for the three-day waiting period. If your disability stretches to 14 days or more, those initial days are owed to you.

This is a frequent source of small but real underpayments. Workers who cross the 14-day threshold are sometimes never paid for the waiting period they are now entitled to, simply because no one went back and corrected it.

Off work longer than two weeks? You may be owed the three-day waiting period that insurers often forget to pay. Talk to our Oregon workers’ comp team about what you are owed.

Full Time-Loss vs Partial Time-Loss

Time-loss is not all-or-nothing. The amount you receive depends on whether you are completely off work or back at reduced capacity.

Temporary total disability

When your doctor authorizes you to be entirely off work, you receive temporary total disability, the full two-thirds wage-replacement benefit. This is the standard time-loss most workers picture, and it continues as long as your physician keeps you off work and your claim remains open.

Temporary partial disability

If you return to work in a lighter-duty or part-time role while still recovering, you may receive temporary partial disability instead. This benefit makes up part of the difference between your reduced earnings and your pre-injury wage. Returning to modified work is generally a good thing, but it changes how your benefit is calculated, and errors in that calculation are common.

The constant in both cases is medical authorization. Time-loss in either form depends on your attending physician documenting your work status, which is why staying connected to your doctor and keeping your paperwork current is so important.

When Time-Loss Benefits Stop

Time-loss is temporary by design, and several events can end it. Payments generally stop when your doctor releases you to your regular work, when you actually return to your job at full wages, or when your claim is closed. The Oregon State Bar’s guide to what workers should know outlines how the temporary-benefit period fits into the larger claim timeline, and the Workers’ Compensation Division’s FAQ publication covers the rules in more depth.

Not every stoppage is correct. Insurers sometimes cut off time-loss based on a disputed medical opinion, a premature release to work, or a claim closure that does not reflect your real condition. When that happens, you have the right to challenge it, and many workers recover benefits that were wrongly halted. Schoenfeld & Schoenfeld regularly takes on exactly these disputes, and the firm’s record of workers’ compensation results reflects how often a cutoff can be reversed.

If your payments stop and you do not understand why, treat that as a signal to get the decision reviewed rather than assume it was final.

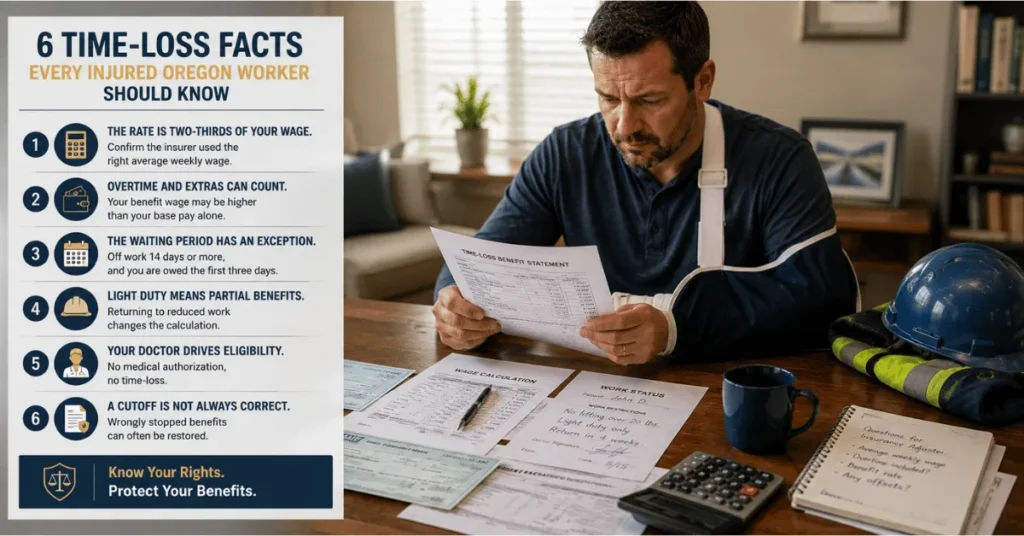

6 Time-Loss Facts Every Injured Oregon Worker Should Know

Time-loss is where the dollars hit your account, so the details are worth committing to memory.

- The rate is two-thirds of your wage. Confirm the insurer used the right average weekly wage.

- Overtime and extras can count. Your benefit wage may be higher than your base pay alone.

- The waiting period has an exception. Off work 14 days or more, and you are owed the first three days.

- Light duty means partial benefits. Returning to reduced work changes the calculation.

- Your doctor drives eligibility. No medical authorization, no time-loss.

- A cutoff is not always correct. Wrongly stopped benefits can often be restored.

These are the points that separate workers who get their full benefits from those who quietly get less.

Conclusion

Time-loss benefits in Oregon exist to keep you afloat while you heal, but only if they are calculated correctly and paid for as long as you are entitled to them. The formula is two-thirds of your wage up to a yearly maximum, the three-day waiting period has an exception worth knowing, and a stopped payment is not always the last word. Checking the math and questioning a cutoff are well within your rights.

Schoenfeld & Schoenfeld has fought for Oregon’s injured workers since 1991, and attorney Steve Schoenfeld has personally handled thousands of workers’ compensation hearings. With a hands-on, small-firm approach and bilingual staff serving Hood River, The Dalles, and Eastern Oregon, the firm focuses on the disputes insurers expect workers to accept, including underpaid and wrongly terminated benefits. This article is general information, not legal advice, and your benefit amount depends on your specific wages and circumstances.

Think your time-loss is wrong or stopped too soon? A complimentary consultation will tell you whether your benefits were calculated and paid correctly, and what to do if they were not. Contact Schoenfeld & Schoenfeld to speak with an experienced Oregon workers’ comp attorney. The consultation is free.